What is Medicare Part B?

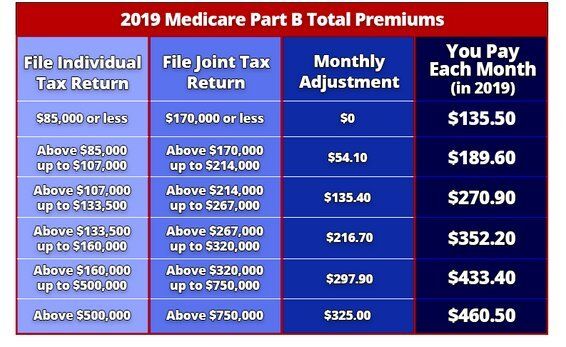

Medicare Part B is part of Original Medicare and covers services and supplies that are medically necessary to treat your health conditions. This can include outpatient care, preventive services, ambulance services, and durable medical equipment (DME). Unlike Medicare Part A, which is premium free for most people, Medicare Part B does require a monthly premium, which is adjusted according to your household income,

and covers up to 80% of your health care costs.

Medicare Part B helps pay for services from doctors and other health care providers, outpatient care, home health care, durable medical equipment (DME), and some preventative services. Medicare Part B preventive services include:

- Abdominal aortic aneurysm screening

- Alcohol misuse screenings & counseling

- Bone mass measurements (bone density)

- Cardiovascular disease and behavioral therapy

- Cervical & vaginal cancer screening

- Colorectal cancer screenings

- Depression screenings

- Diabetes screenings

- Diabetes self-management training

- Glaucoma tests

- Hepatitis C screening test

- HIV screening

- Lung cancer screening

- Mammogram screening

- Nutrition therapy services

- Obesity screenings & counseling

- One-time “Welcome to Medicare” preventive visit

- Prostate cancer screenings

- Sexually transmitted infections screening & counseling

- Shots: Flu, Hepatitis B, Pneumococcal shots but not Shingles

- Tobacco use cessation counseling

- Yearly "Wellness" visit

Special Note: Medicare DOES NOT cover Shingles shots.

For a full list of preventive services covered under Medicare Part B, refer to the Medicare handbook, "Medicare and You."

Eligibility for Medicare Part B

Anyone who is eligible for premium-free Medicare Part A is eligible for Medicare Part B by enrolling and paying a monthly premium. If you are not eligible for premium-free Medicare Part A, you can qualify for Medicare Part B by meeting the following requirements:

You must be 65 years or older.

You must be a U.S. citizen, or a permanent resident lawfully residing in the U.S for at least five continuous years.

You may also qualify for automatic Medicare Part B enrollment through disability. If you are under 65 and receiving Social Security or Railroad Retirement Board (RRB) disability benefits, you will automatically be enrolled in Medicare Part A and Part B after 24 months of disability benefits. You may also be eligible for Medicare Part B enrollment before 65 if you have end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (also known as ALS, or Lou Gehrig's disease).

Medicare Part B premiums

Medicare Part B premiums may change from year to year, and the amount can vary depending on your situation. For many people, the premium is automatically deducted from Social Security benefits. If you are receiving Social Security, Railroad Retirement Board, or federal retirement benefits, your Part B premium will be deducted directly from your monthly benefit. If not, you will be sent a bill every three months.

When to enroll in Medicare Part B

Unless you are receiving retirement benefits before age 65 or qualify for Medicare through disability, you will need to sign up for Medicare Part B during your initial enrollment period (IEP). This is the seven-month enrollment period that begins three months before you turn 65, includes the month you turn 65, and ends three months later. Your Medicare coverage start date will depend on which month you signed up during initial enrollment. If you have health coverage through an employer health plan, you may choose to delay enrollment since Medicare Part B comes with a monthly premium. If you delay your Part B you will have an eight month special enrollment period (SEP), once you retire, to sign up and to choose a Medigap plan to supplement the gaps that Parts A & B do not cover

If you do not enroll during your initial enrollment period (IEP) and do not qualify for a special enrollment period (SEP), you can also sign up during the Part B general enrollment period (GEP), which runs from January 1 to March 30. You may have to pay a late enrollment penalty (LEP) for not signing up when you were first eligible, and your Part B coverage will not be effective until July of that year. Your monthly premium may be 10% higher for each 12-month period that you were eligible, but did not enroll in Part B.

You can apply for Medicare through Social Security, either in person at a local Social Security office, through the Social Security website https://secure.ssa.gov/iClaim/rib

or by calling 1-800-772-1213 (TTY users 1-800-325-0778) from 7AM to 7PM, Monday through Friday.

Keep in mind that once you are both 65 years or older AND have Medicare Part B, your six-month Medicare Supplement (aka Medigap) Open Enrollment Period begins. This is the best time to purchase a Medicare Supplement plan because during open enrollment, you have a "guaranteed-issue right" to buy any Medigap plan without medical underwriting or paying a higher premium due to a pre-existing condition. Once you are enrolled in Medicare Part B, be careful not to miss this one-time initial guaranteed-issue enrollment period for Medigap.

Delaying Medicare Part B enrollment

Because Medicare Part B comes with a monthly premium, some people may choose not to sign up during their initial enrollment period if they are currently covered under an employer group plan (either their own or through their spouse's employer).

If you are still working, you should check with your health benefits administrator to see how your insurance would work with Medicare. If you delay enrollment in Medicare Part B because you already have current employer health coverage, you can sign up later during a Special Enrollment Period (SEP) without paying a late penalty. After your employer health coverage ends or your employment ends (whichever comes first), you have an eight-month special enrollment period (SEP) to sign up for Part B without a late penalty.

Keep in mind that retiree coverage and COBRA are not considered “creditable” health coverage (prescription drug coverage that is equal to or better than Medicare) based on current employment and would not qualify you for a special enrollment period. If you have COBRA after your employer coverage ends, you should not wait until your COBRA coverage ends to sign up for Medicare Part B. Your eight-month Part B special enrollment period begins immediately after your current employment or group plan ends (whichever comes first). This is regardless of whether you get COBRA.

For additional information about Medicare Part benefits feel free to contact me at 408-849-4460 or email me at julie@jbinsurance.biz